In 1990, life expectancy in our country was at 58 years, while the retirement age was between 55 – 60 yrs in various state and central government jobs. Many people died before they retired. We had movies on withdrawal symptoms after retirement and how the erstwhile who’s who coped up with inactivity and lack of importance. Since that generation had steady pension and a huge Provident Fund, usually financial trouble was not one of the problems they faced post retirement. This was despite being predominantly a single income family with several dependents.

This could be a million rupee question based on what is it you intend to buy or rent? In this post I’ll try to cover various category of assets and both financial and non financial aspects of this question.

Rent Vs Buy

Immovable Assets :

For Most of us, the only immovable asset we will own is our home or utmost a piece of land. We have all been told stories of how somebodies grandfather bough a tiny piece of land several years ago for a tiny pittance, far away from the city and lo right now it is the heart of the expanded bustling city, fetching several crores. We feel inspired by the story and go home hunting.

Warning: This book is an advanced read even for finance professionals. You must have basic knowledge on capital markets to be able to understand and appreciate the book. Like high echelons of Carnatic music, this book is a God send for those obsessed with return on and of their investment, but most others may be unable to appreciate the finesse of the mentioned points.

We have seen finance experts like Dave Ramsay tell us to cut up our credit cards. We have seen how delinquent home loans not only caused people to lose their homes but also a systemic crisis that spread across several financial institution and countries during 2008. Repossessed cars and two wheeler are common in many low income households. To add to this trouble student loan defaults have become high all over the world as the income opportunities often don’t match up with the cost of some of these courses.

So is debt a bad thing? Should we indeed cut up credit cards? Save for 15+ years to buy a home. Never take a loan in our life?

From Shylock of ‘Merchant of Venice’ to today’s bank that offer Personal loans and credit cards with dubious terms the bankers have been portrayed as Vultures. It is often joked ‘Banks will only lend money to those that don’t need them.’. Are these Financial institutions just vultures that serve no real need?

‘A penny saved is a penny earned’ is an adage you will hear so often that its sheer repetition will make you believe it to be true. But is it really true? Sure, money not spent right now is sitting to be spent on something else later. Economics defines this as opportunity cost. But in this article, I am going to argue against ‘thrifty saving’ as a way to ‘grow your money’ or to ‘get and live rich’. Continue reading Why thrifty saving is not the same as investing

This is one of the oldest books on investments and personal finance that has survived time and covers all the basic knowledge required for a beginner wealth builder. The fable covers simple advice to start wealth building to most common mistakes committed by those in their journey to financial independence.

A book of the title ‘Automatic Wealth‘ is sure to get interest from many, however the this is no get rich quick with no work book. Some specific advice in the book, revolves around USA, however the basic premises of the book is applicable across countries and markets.

The book breaks down the process of wealth building into six steps:

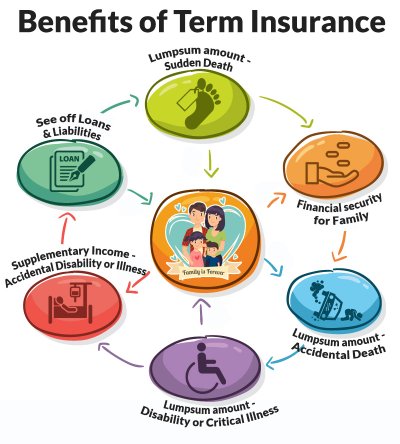

India has one of the lowest penetration of life insurance of under 3.5 %. But many of us have a number of policies for which we dutifully, pay premiums every year but don’t know for sure if we it is useful or not. Even as a finance professional, I have made a number of those rookie mistakes, so I can totally understand how gullible one can be to those pitches.

So let us examine, some basic questions to help us guide through these decisions.

What is insurance?

Insurance contract ensures the policy holder is compensated for his loss when a certain event happens. So extending this definition, we can say a life insurance is a monetary compensation for loss of earning potential due to death or disability.

This simple definition provides us all the necessary understanding required to evaluate a policy. So let me try and break this done into a checklist.